95. Squeeze to Please

A field guide to the four holding companies still standing; who’s winning, who’s hiding, who’s quietly for sale, and why the biggest ad budgets now belong to the AI companies holdcos can’t sell to.

Hello.

You may have noticed The Ad Stack went dark for a month. No worries. I wasn’t acquired, I didn’t pivot to a Substack about sourdough, and no, the algorithm didn’t bury me. I simply did what every great brand does when engagement dips: I called it “intentional silence” and added it to the content calendar retroactively.

The official story is that I was “heads-down on strategy.” The real story is that I opened a blank draft roughly forty times, wrote the word “So,” stared at it like it owed me money, and closed the laptop. Turns out the hardest part of a publishing schedule is the publishing. And the schedule.

But here’s the thing about going quiet in a business built on never shutting up: absence is just scarcity marketing you didn’t mean to do. So consider this my triumphant relaunch. Same newsletter, now with a full month of pent-up opinions and zero new excuses.

I sat on this edition for a couple of weeks; repeatedly re-reading. Effectively killing it. Someone asked me, “So when the **** are you sending something out?!”

That said, following is a ****-load of information. Feel free to use your expletive of choice. Let’s look at how the holding companies might be doing. I’ve got no dog in this fight.

Let’s get into it.

The Funny Part

The funny part about the Q1 2026 advertising holding-company earnings cycle isn’t the numbers. It’s that one of the four CEOs running these things skipped her own earnings call.

Cindy Rose, eight months into the WPP top job, opted out of presenting the company’s 8.9% revenue decline to analysts. The official line was that the strategy update was scheduled separately. The unofficial line is that there is nothing reassuring to say when your top 25 clients have shrunk 9.4% year-over-year and your stock is down roughly 51% in twelve months.

What follows is what the trade press has been too polite, or too dependent on holdco ad spend, to lay out plainly. The numbers are real. The conclusions are speculative. The satire is what’s left when you put both side by side.

1. The Standings

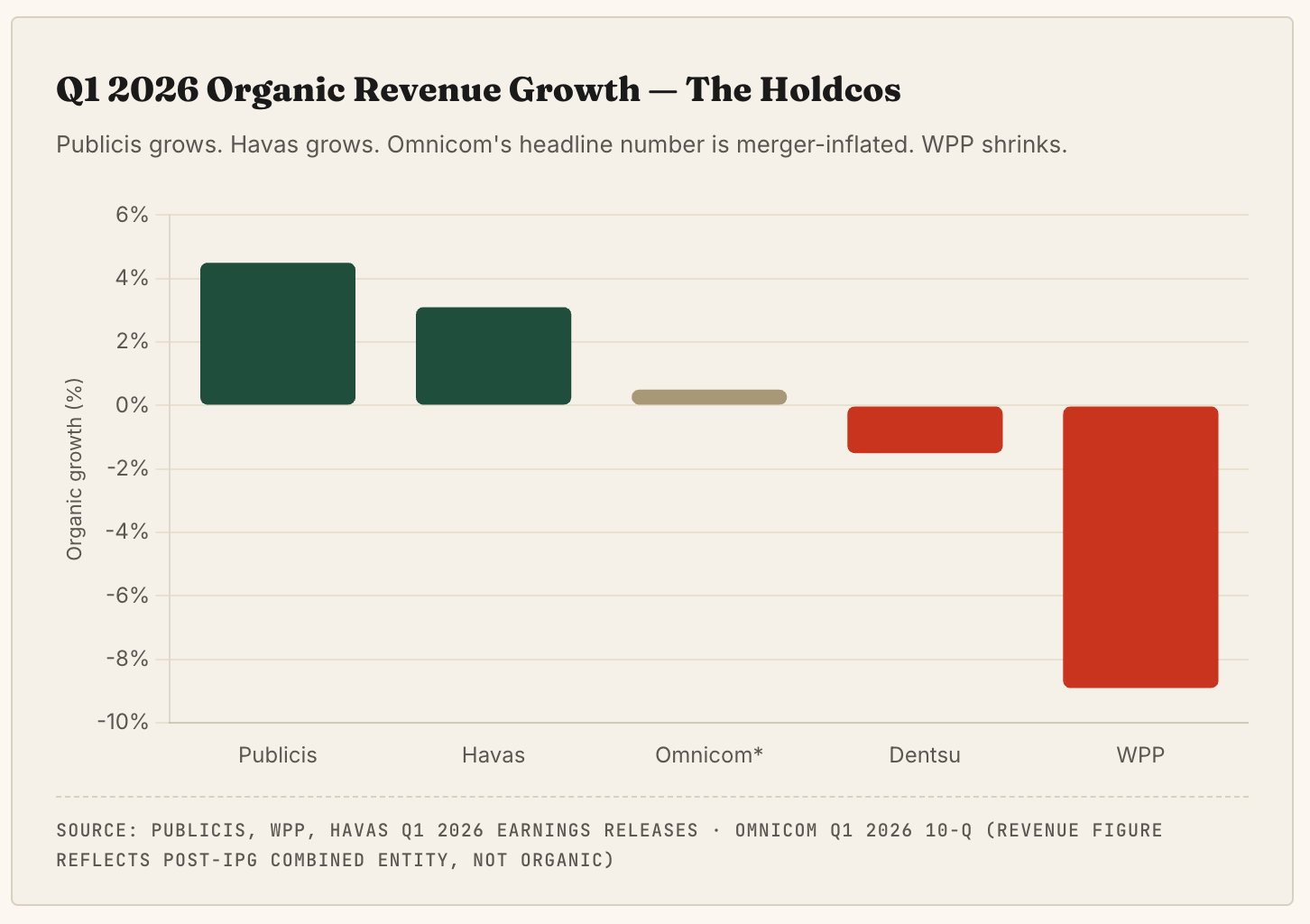

The Q1 Scoreboard Says What the Press Releases Don’t

If you read individual earnings releases, every holdco is “executing on transformation,” “investing in AI capabilities,” and “pleased with progress.” If you line up Q1 2026 organic growth side by side, you get a different story.

Publicis grows. Havas grows. Omnicom’s headline number is merger-inflated. WPP shrinks.

The gap between Publicis and WPP in a single quarter is roughly 13 percentage points. In an industry whose long-run nominal growth is 3–5%, that is not a “transformation gap.” That is one company growing and one company falling out of an airplane.

Sadoun is, of course, talking his book. He is also factually correct about all three things.

2. WPP Skipping Your Own Earnings Call Is, At Minimum, A Choice

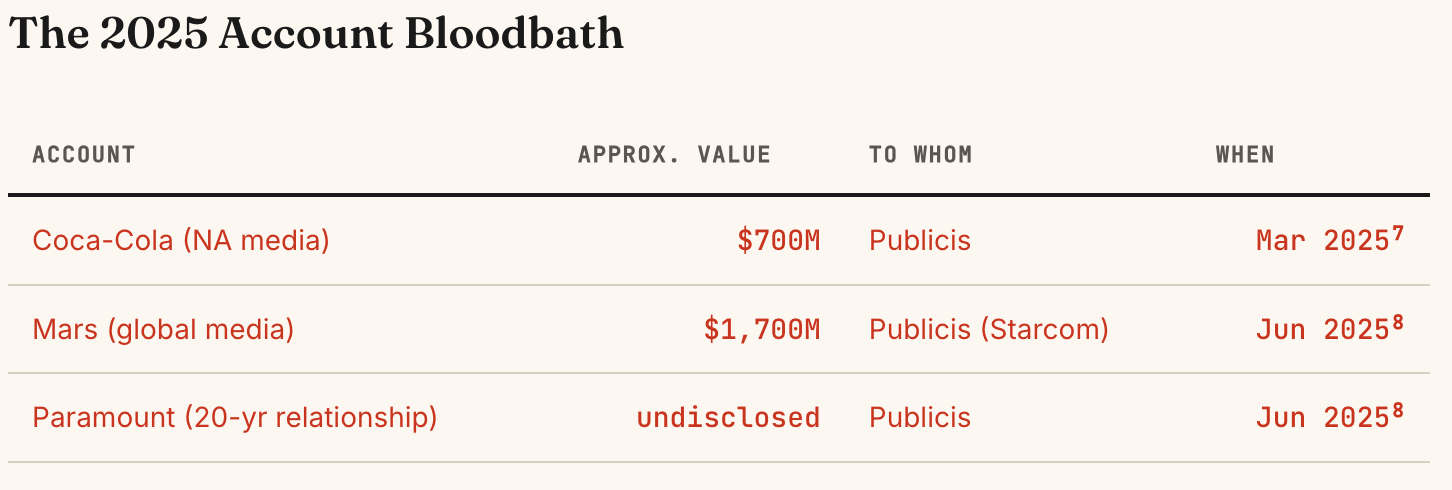

The story being told about WPP, that it is mid-turnaround under new leadership, buries the real story. WPP has lost the three biggest media accounts in the industry in roughly fifteen months, and there is no plausible read of the numbers in which that doesn’t matter.

The 2025 Account Bloodbath

WPP’s response to losing the Mars account was, and this is real, to publicly question Publicis’s “ad quality,” as described below:

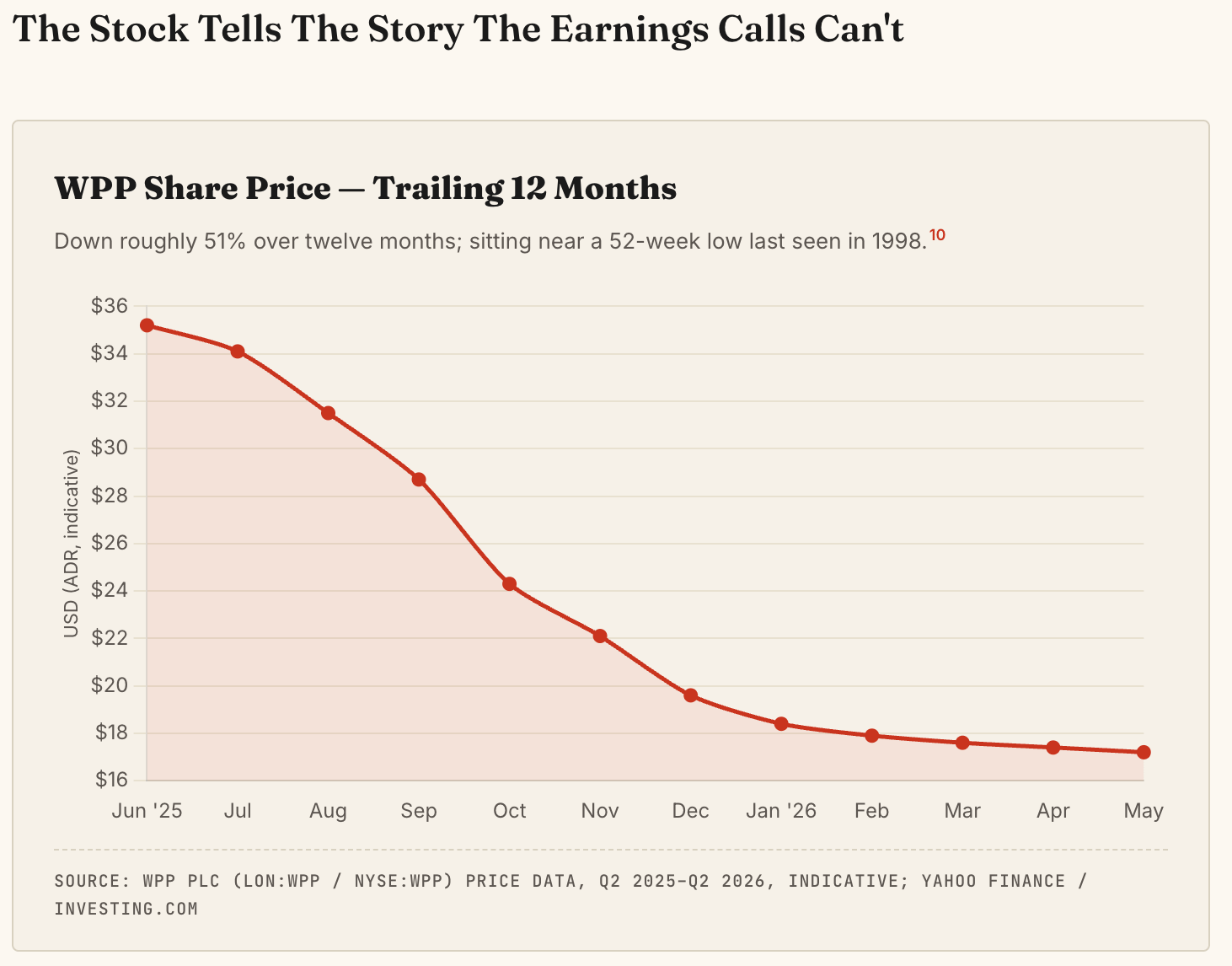

The Stock Tells The Story The Earnings Calls Can’t

WPP Share Price — Trailing 12 Months

Down roughly 51% over twelve months; sitting near a 52-week low last seen in 1998.

The shareholder return number is the one nobody at WPP wants on a slide: three-year total return is approximately negative 60%. In the same period, the S&P 500 returned roughly +28% and Publicis Groupe roughly +35%. WPP is not underperforming the market; it is underperforming a savings account.

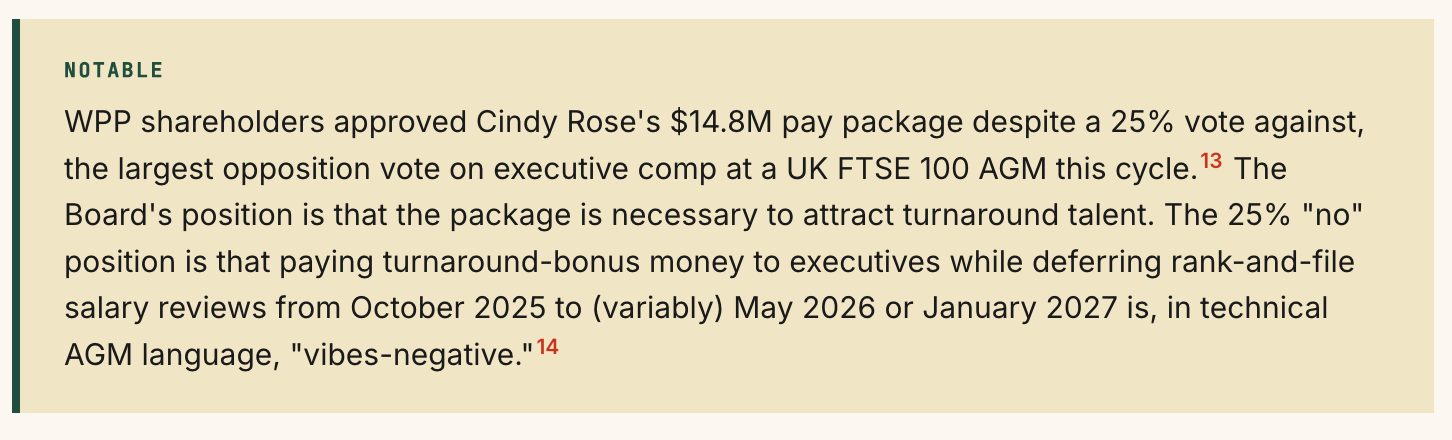

Elevate28: The Plan, Slightly Late

Rose’s restructuring plan, “Elevate28,” targets $675M in gross annual savings by 2028. The plan is rational. The plan is also, with respect, Omnicom’s playbook from December 2024 with a one-year time-lag and a new color palette. Omnicom announced a comparable program coupled to a transformative acquisition. WPP is announcing a comparable program coupled to losing accounts.

Analyst consensus is that WPP needs to shrink headcount by 10–15% in 2026. WPP Media (the rebranded GroupM) reportedly started layoffs days after the rebrand was announced; which is the corporate-comms equivalent of finishing your toast at the rehearsal dinner and then immediately filing for divorce. VML separately cut North American staff, citing a “shift in client needs.” The shift in question is mostly that the clients are at Publicis now.

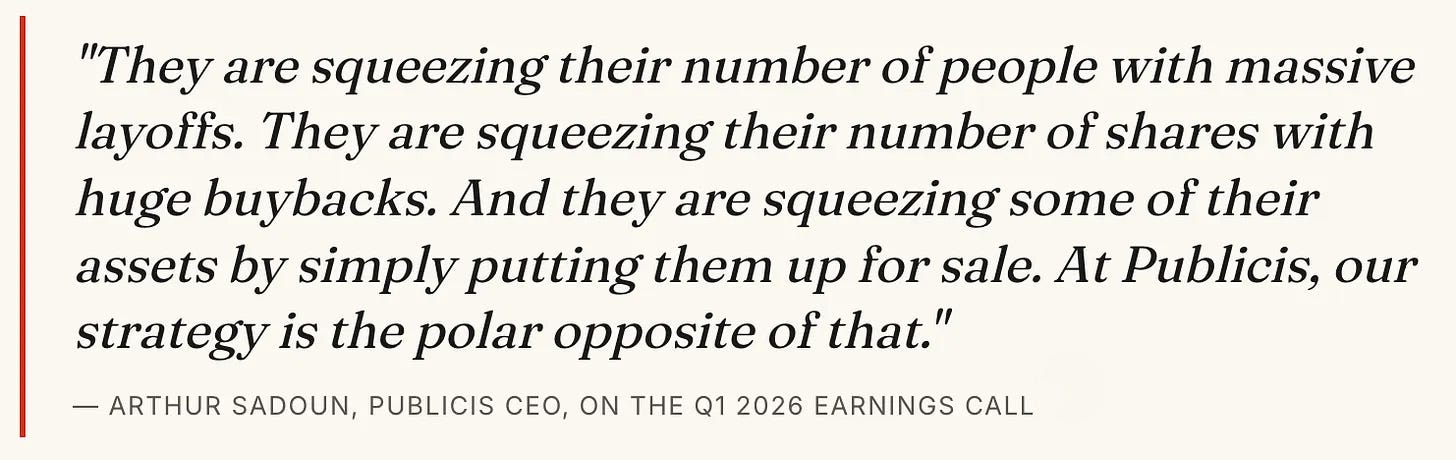

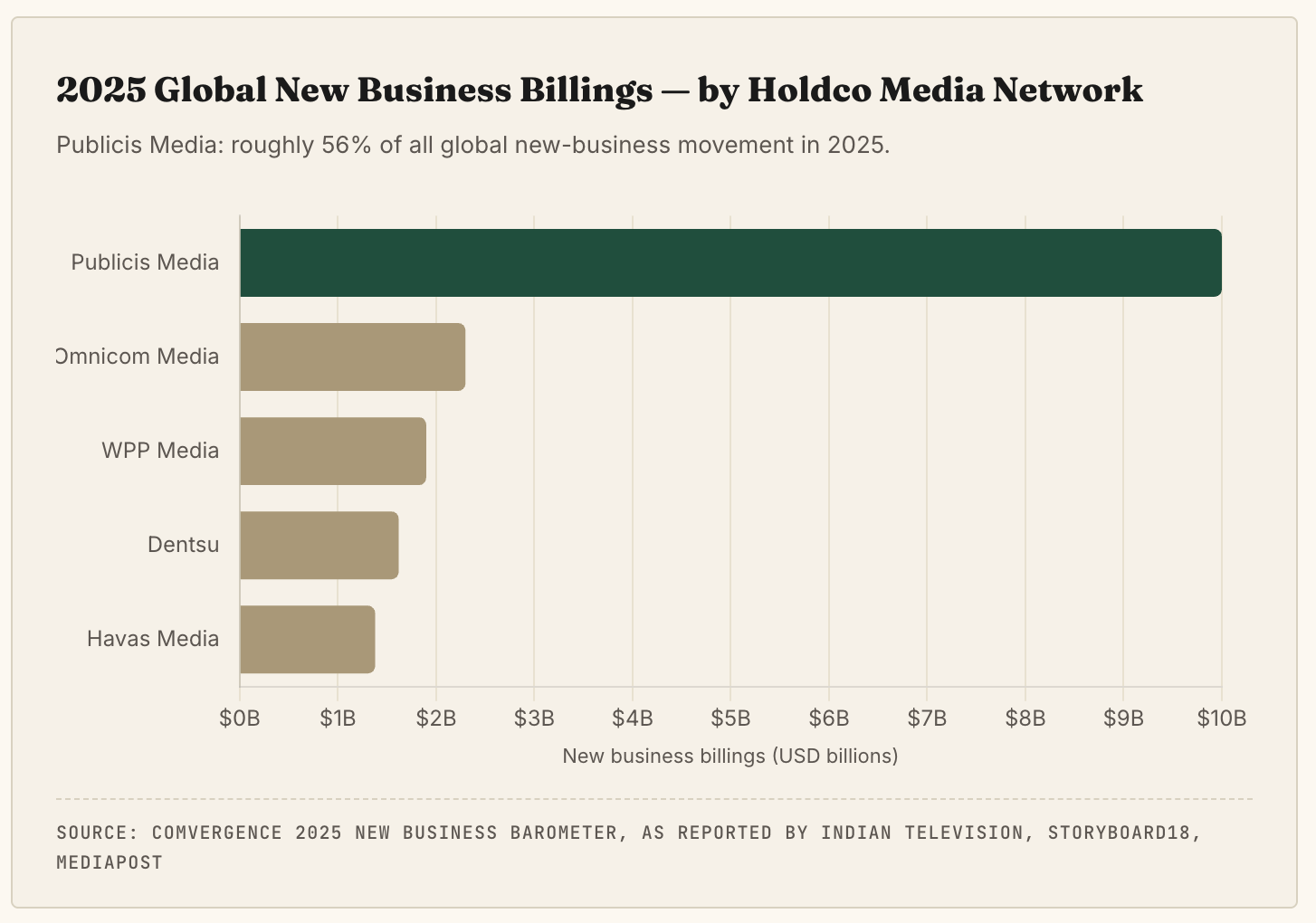

3. Publicis The 56% Solution, Or: How To Win By Not Tripping

Publicis Media captured roughly 56% of all global new business billings in 2025, per COMvergence — about $10 billion in new client billings, or close to a third of all media spend that changed hands in the year. Starcom alone won $2.7B, including the Mars and Aldi accounts. Spark Foundry added another $2.1B. This is not a “Publicis is doing well” market share. This is a “Publicis is the market” share.

Why Publicis Won — A Decision Made in 2019

Almost everything visible in 2026 is a consequence of one decision Sadoun made in April 2019: paying $4.4 billion for Epsilon, the loyalty/identity/first-party data platform that Wall Street analysts at the time openly called overpriced and strategically confused. The CNBC headline was literally “analysts skeptical.” Sadoun closed the deal anyway.

Seven years later, Epsilon is the backbone of CoreAI — Publicis’s identity graph and AI activation layer — and it is the reason Coca-Cola, Mars, and Paramount left WPP. WPP, in 2019, was busy unwinding Sir Martin Sorrell’s empire and could not have spent $4.4B on identity infrastructure if it wanted to. The fact that one CEO was willing to take a strategic bet that looked obviously wrong at the time, and the other was managing a succession crisis, explains seven years of relative trajectories better than any AI narrative ever will.

This is the boring truth that doesn’t make Cannes panels: the AI race in adland was effectively won in 2019, by a French CEO buying a Texas data company nobody could justify on a DCF.

The Sadoun Doctrine, Stated Plainly

On the Q1 2026 call, Sadoun did something unusual for a public-company CEO: he framed his entire 2026 thesis around not doing what his competitors are doing.6 No mega-acquisition. No principal media plays (he ruled out the Omnicom-style media arbitrage model in February20). No headcount squeezing. The pitch is essentially: “We did the painful work between 2017 and 2022. The rest of you are doing it now. We’re not going to do it again on your schedule.”

Whether the strategy holds depends on whether AI actually creates the productivity gains Sadoun is betting it does. If it doesn’t, his cost base is the most exposed in the industry. If it does, and the early CoreAI utilization data suggests it does, then we’re heading into a winner-take-most decade.

04: Omnicom + IPG

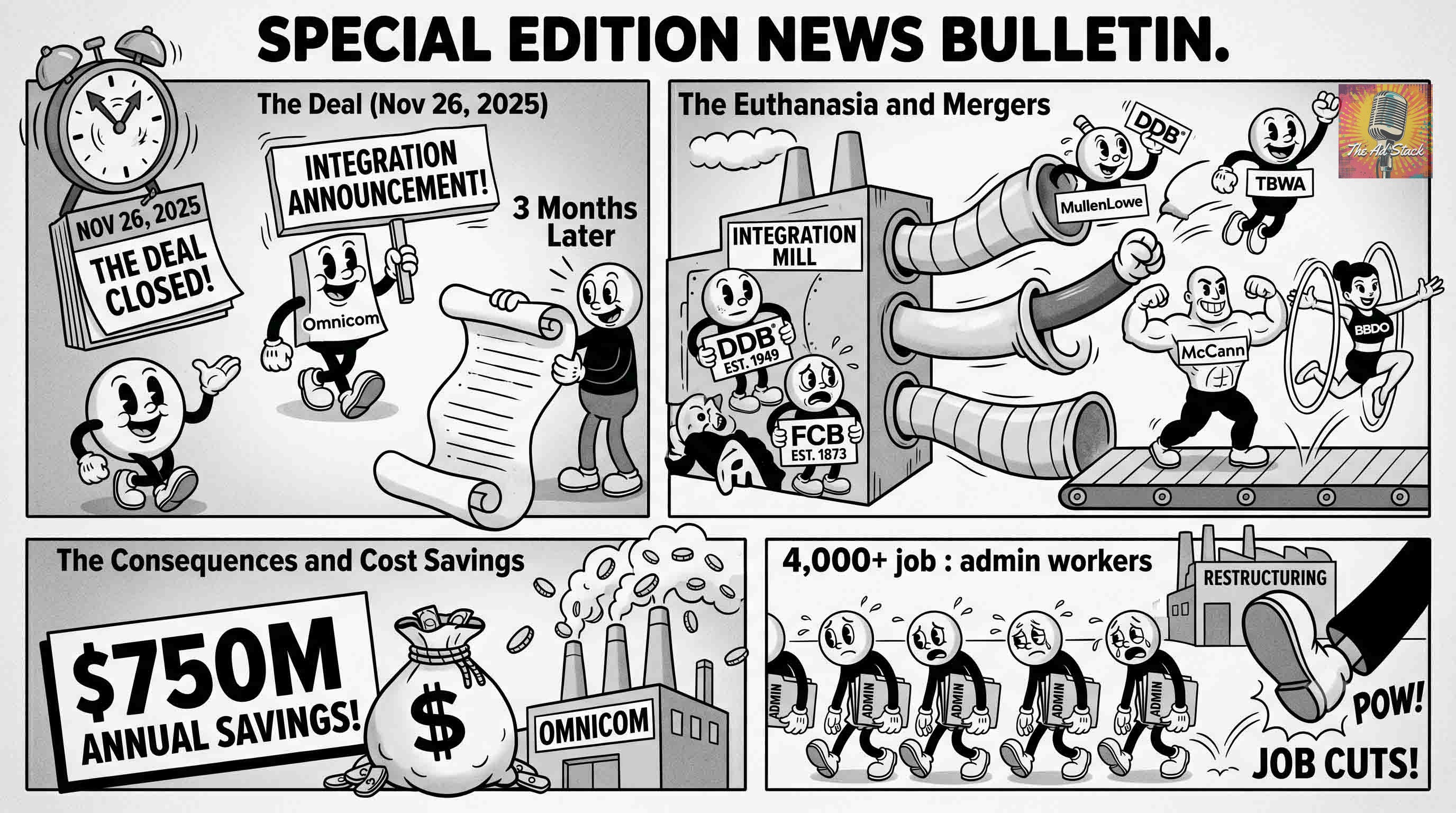

The Merger Closed. The Hard Part Is Starting.

The deal closed November 26, 2025. Three months later, Omnicom announced the most aggressive integration anyone has seen out of a holdco merger in decades: DDB (founded 1949), FCB (rooted to 1873), and MullenLowe are being euthanized in the first half of 2026, folded into TBWA, McCann, and BBDO respectively. Total job cuts: 4,000+, mostly admin. Targeted savings: $750M annually, above original guidance.

Ruhanen’s “relevance, not legacy” framing is the most quoted line in the trade press this quarter. It is also a confession dressed as a strategy. Translation: we cannot afford the brand equity of three networks we no longer have a thesis for, so we’re going to brand-equity-launder them into BBDO. The clients of DDB, FCB, and MullenLowe are about to discover whether they were paying for the agency or the logo.

Omnicom’s reported Q1 2026 revenue of $6.2B is up $2.6B — but the increase is mechanically the IPG bolt-on. Operating margin compressed from 12.3% to 10.4% on $59M of integration costs, $4M of severance, and $34M of disposition losses.25 The merger math depends on hitting the synergy number. The synergy number depends on not losing the people you need to keep.

05: Dentsu (and the Havas merger circus)

For Sale: One Slightly Used Network, Lightly Internationalized

Dentsu, the Japanese holdco that for the last decade tried to be a global player by acquiring Aegis and Merklel; quietly disclosed in August 2025 that it had hired Mitsubishi UFJ Morgan Stanley and Nomura to explore strategic options including a sale of its international business. Forrester’s reaction to the news was, in essence, “we told you so.” Dentsu’s international integration has been visibly underperforming for three years.

The crown jewel of any Dentsu international sale is Merkle, the data consultancy acquired in 2018. Merkle is essentially Dentsu’s answer to Epsilon. Which is to say, the asset that Publicis already won the war with. Whoever buys Merkle is buying a second-place data infrastructure in a game where the first-place player is six years ahead.

The Havas Subplot

In November 2025, The Times reported that Havas, controlled by the Bolloré family, was in “very serious” early-stage talks about WPP, potentially involving a minority stake purchase. Within days, Havas CEO Yannick Bolloré denied the talks in a staff memo, while carefully leaving the door open to “larger acquisitions aligned with our strategy.”

“We are not in discussions with WPP” is a sentence that means three different things depending on tense interpretation. It does not mean “we have never been in discussions with WPP” and it does not mean “we will never be in discussions with WPP.” The Havas CFO has separately confirmed interest in Dentsu’s international business.

If Dentsu sells its international arm and Havas buys it (or buys WPP’s media business, or some combination), the global advertising industry collapses from five holdcos to four — or, more interestingly, to three plus a holdco for the remainders. By 2027 there is a non-trivial probability the league table reads: Publicis, Omnicom-IPG, [whoever ends up owning the WPP/Dentsu/Havas residue], and the AI platforms.

06: The Real Disruption

Your Biggest Advertiser Is Now An AI Company

The narrative in trade press is that “AI is disrupting the holding companies.” The numbers say something more specific and more interesting: AI gave Omnicom and Publicis a permission structure to do the consolidation they already wanted (admin, middle management, production). The job cuts would have happened anyway. AI is the macro story that makes them socially acceptable.

The actually disruptive AI story for the holdcos is on the other side of the ledger. It is on the media buyer side, not the agency side.

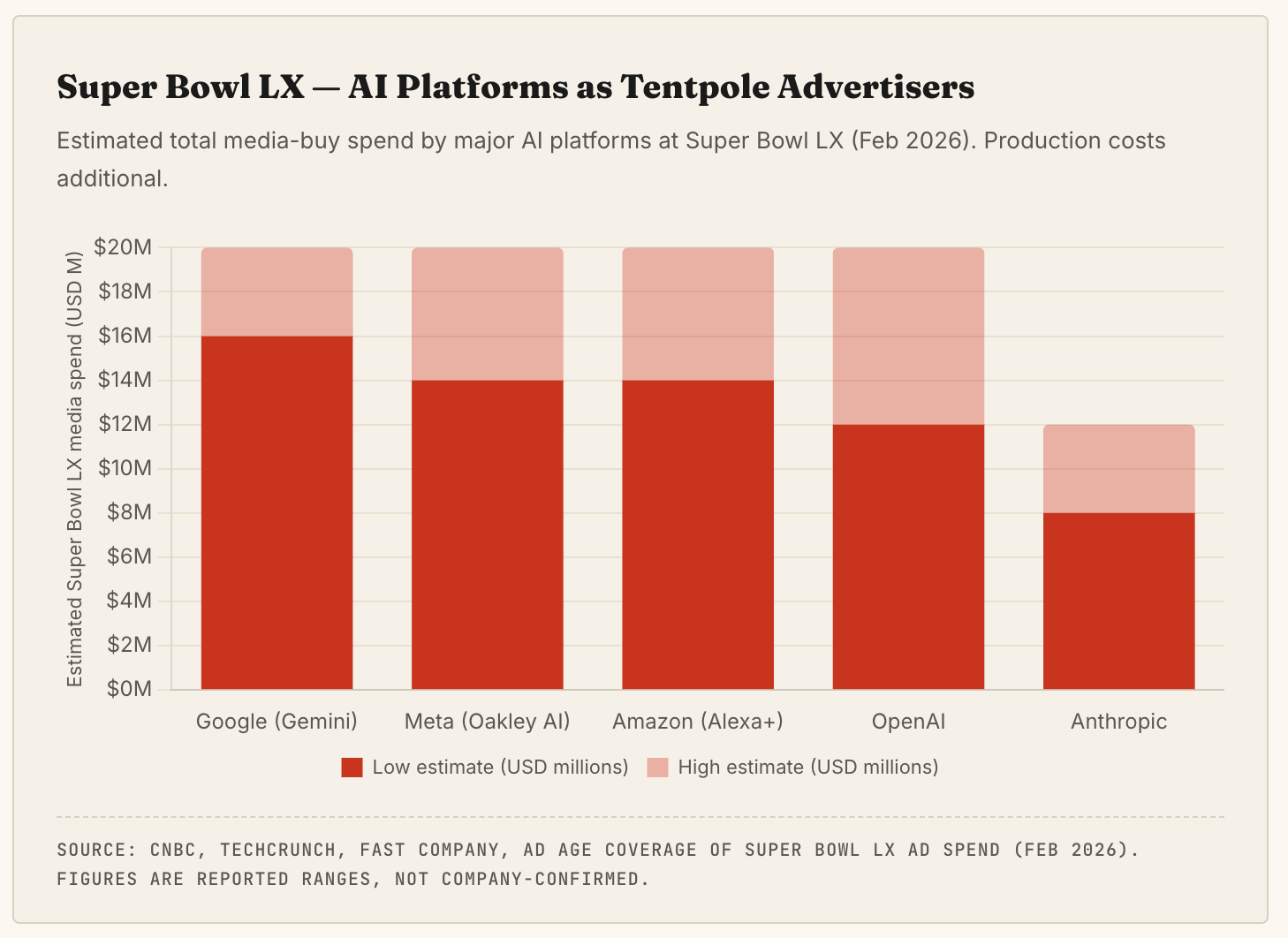

Super Bowl LX, February 2026

Of the 66 commercials that aired during Super Bowl LX, 15 — nearly a quarter — featured AI in some way.31 OpenAI, Anthropic, Google (Gemini), Amazon (Alexa+), and Meta (Oakley Meta glasses) all bought ad time. Reported media buys ran $8–20M per company.

The Anthropic ads, four satirical spots tagged “Ads are coming to AI,” were a pointed shot at OpenAI’s plans to monetize ChatGPT with ads. Sam Altman called them “funny but clearly dishonest.” Anthropic’s daily-active-user count jumped 11% post-game, the largest lift in the AI cohort per BNP Paribas data.

Why This Is The Story That Matters

The Super Bowl is the closest thing the U.S. ad market has to a power ranking. Historically, the dominant Super Bowl advertisers have been CPG (Anheuser-Busch, P&G), automotive, telecom, and the occasional tech IPO splurge. Those brands were, almost without exception, holdco clients.

In 2026, roughly a quarter of Super Bowl ads were AI platforms. The AI platforms are not holdco clients. They run their creative in-house, or with boutique production shops, or — increasingly — with AI-generated work made on their own models. They buy media programmatically, not through holdco media networks. The holdcos do not sit in the middle of the largest emerging ad-spending category in television.

The structural implication: if the next ten years of upper-funnel media growth is AI-platform brand-building (which it appears to be), the holdcos are not the gatekeepers to it. They are vendors at the periphery of it, hoping to win occasional production work that presently keeps smaller shops and prodco’s busy. The platforms they used to mediate access to — Meta, Google, Amazon — are themselves now the buyers, building first-party creative pipelines.

This is the inversion that the trade press hasn’t fully metabolized. Omnicom and Publicis can consolidate, cut costs, and ship AI-augmented creative all day. None of that changes the fact that the fastest-growing category of TV advertiser in 2026 doesn’t need them.

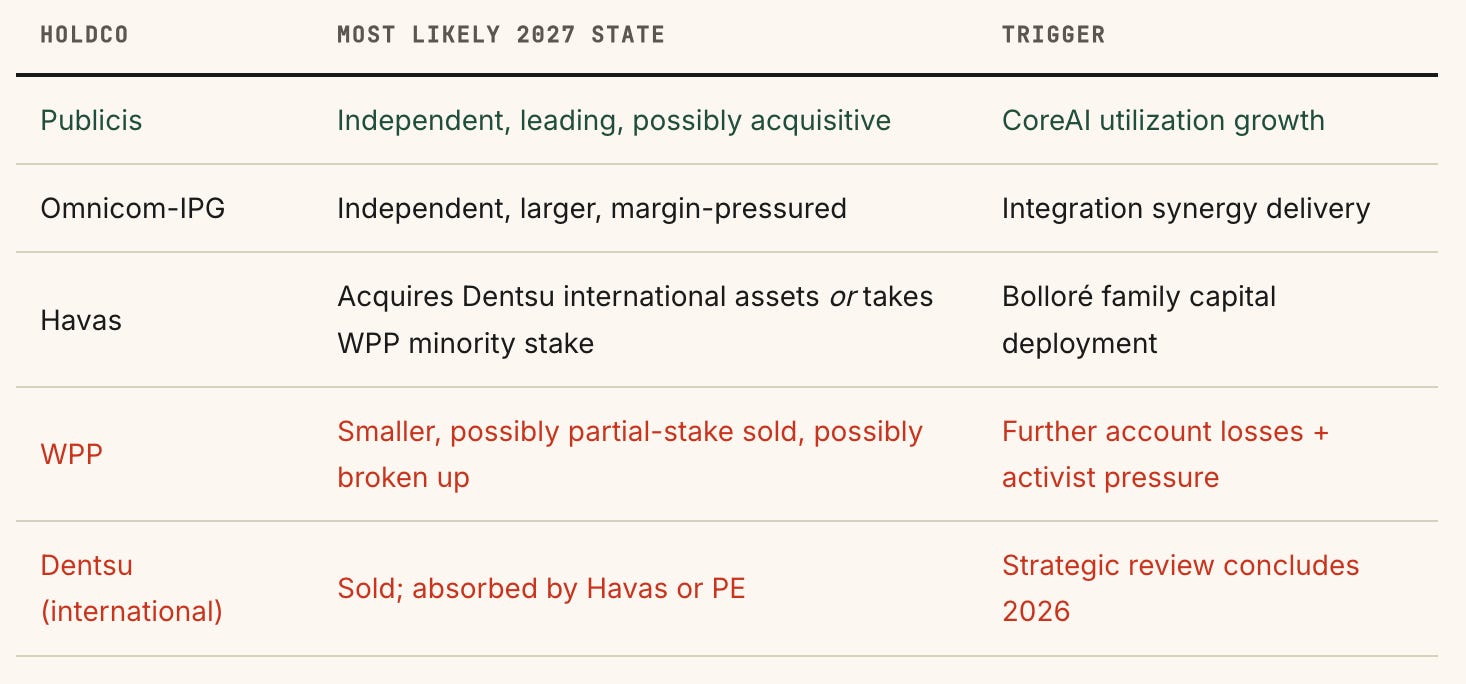

07: The Forecast

A Three-Holdco World by 2027, And What It Costs To Get There

Here is the forward-looking call, stated with the appropriate disclaimers about forecasting in a market this turbulent

What this means for marketers:

If you are a CMO at a top-50 global advertiser, your three-year planning horizon should assume your current holdco-of-record might not exist in its current form by 2028. Publicis is the safe play if you can stomach the price. Omnicom is the operational risk play (integration). Anyone else is, charitably, an option position on consolidation.

What this means for the AI platforms:

You are now in the media business; not as advertisers buying media, but as buyers competing with the holdcos for the relationships that used to sit between brand and consumer. The interesting question for 2027 is whether OpenAI, Anthropic, Google, and Meta start acquiring agencies, or whether they conclude that the agencies are the obsolete intermediary they’re explicitly trying to sidestep.

My bet:

They don’t acquire the agencies. They hire from the agencies, build in-house, and let the holdcos shrink into the high-touch, high-craft, high-margin work that AI can’t yet do. Which, by the way, is a real business. It’s just a smaller one than the four current incumbents are built for.

For The Ad Stack readership:

The thesis here will hold for another 1–2 quarters; after that, Dentsu’s strategic review concludes and the next domino falls. It is opinion and satire. I could be wrong. So could a lot of people.

Sources & Footnotes

Adweek — “WPP Revenue Falls 8.9% as CEO Cindy Rose Opts Out of Q1 Earnings Call”

StockInvest.us / WPP plc price data — TTM decline approximately 51%

Campaign US — “Publicis hits 4.5% Q1 growth as Sadoun rejects rivals’ ‘squeeze’ tactics”

Adweek — “Omnicom to Cut 4,000 Jobs, Retire FCB, DDB, and MullenLowe”

Indian Television / COMvergence — Publicis Media tops 2025 global new business rankings with $10B

Adweek — “Arthur Sadoun Won’t ‘Squeeze to Please Wall Street’ in the Age of AI”

The Drum — Coca-Cola’s $700m N.A. media account moves to Publicis (March 2025)

Social Samosa — Publicis Groupe bags Mars’ $1.7B global media account, ends WPP’s run

eMarketer — “WPP hits Publicis over ad quality after losing $1.7 billion Mars account”

MM+M — “WPP stock plunges 16% to lowest level since 1998 after fresh Q3 downgrade”

Storyboard18 — WPP shareholders approve Rose’s $14.8M pay despite 25% opposition

BW Marketing World — WPP pushes global salary reviews under Rose’s transformation plan

Digiday — “WPP’s ‘unacceptable’ results show scale of turnaround challenge”

Ad Age — “VML lays off staff in North America, citing shift in client needs”

CNBC — “Publicis’ $4.4 billion acquisition of Epsilon: analysts skeptical”

Publicis Identity & CoreAI — overview of the post-Epsilon identity/AI stack

VideoWeek — “Publicis Groupe says Yes to M&A, No to Principal Media in 2026”

adobo Magazine — Omnicom shuts DDB, FCB, MullenLowe post-IPG

Campaign US — Omnicom shake-up, 4,000 jobs cut, $750M+ savings target

The Drum — “Troy Ruhanen: DDB axe & restructure based on ‘relevance, not legacy’”

Omnicom Q1 2026 10-Q — revenue, integration costs, margin compression

BestMediaInfo — Havas in early talks to acquire stake in WPP (Times report)

Tech Brew — Super Bowl 2026 had a lot of AI and tech ads (15 of 66 commercials)

CNBC — Anthropic +11% DAU post-Super Bowl, per BNP Paribas data